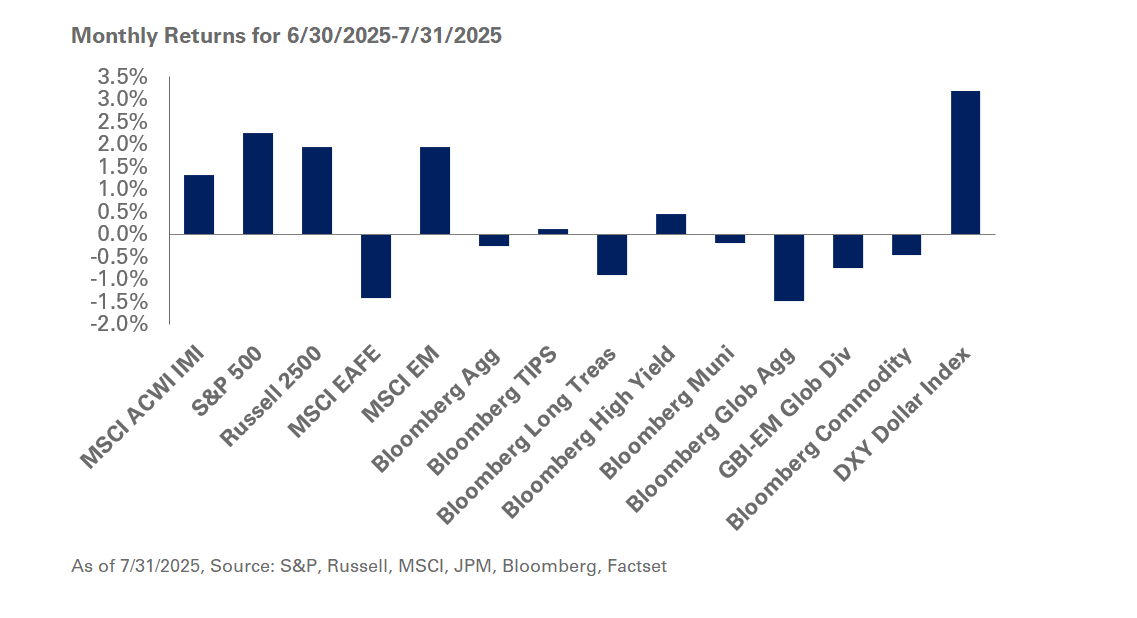

In July 2025, U.S. stock markets reached unprecedented levels, with both the S&P 500 and the NASDAQ setting new all-time highs. Much of this growth was attributed to impressive corporate earnings, with over 80% of companies surpassing earnings expectations. "The S&P 500 gained 2.2%, led by growth stocks, while small-cap equities represented by the Russell 2000 Index climbed 1.7%. However, they remain significantly behind large-cap stocks this year," said a market analyst.

The performance of international equities offered a mixed picture. The MSCI EAFE Index dropped by 1.4% in July, weighed down by the declining values of the euro, sterling, and yen. In contrast, emerging markets thrived thanks to a rally in Chinese equities, highlighting the regional disparities in market performance.

On the economic front, the U.S. made headlines with new trade agreements with notable partners, including Japan and the European Union. The U.S. experienced a robust 3% annualized economic growth rate in the second quarter, a result of increased consumer spending alongside a reduction in imports. As part of a closely watched Federal Reserve meeting, interest rates were kept steady, despite dissent from two members advocating for a rate cut.

However, the July jobs report delivered a stark reality check with the addition of only 73,000 new non-farm payroll jobs, well below analyst expectations. "The adjustments to May and June figures, down by 258,000 jobs, suggest a troubling trend in the labor market," said a labor market economist. Additionally, the three-month average indicated a growth of just 35,000 jobs, marking the largest downward revisions since the late 1970s, suggesting potential vulnerabilities ahead.

"The adjustments to May and June figures, down by 258,000 jobs, suggest a troubling trend in the labor market,"

This weak jobs report now places critical focus on the labor market, trade policy, and forthcoming Fed meetings. According to a financial analyst, "The implications from the jobs report may lead to significant revisions in the market’s expectations for Federal Reserve rate cuts in 2025, particularly as we approach the Fed's meeting in September."

July also saw a downturn in fixed-income returns as interest rates saw a slight increase. The yield on the 10-year Treasury rose to 4.36%, leading to negative returns across Treasury indexes. "While investment-grade and high-yield bonds experienced some relief from a decrease in credit spreads, the upward trend in Treasury rates served as a headwind, with the investment-grade credit index gaining just 0.1% and high-yield bonds improving by 0.5%," noted a bond market strategist.

Within the commodity sector, performance was mixed. Oil prices for WTI Crude surged by 4.5%, closing July just below $70 a barrel. Gold, on the other hand, enjoyed a positive month with a return of 1.4%, cumulatively up over 25% for the year. Meanwhile, the REIT sector continued to lag, down 1% for the month and showing minimal performance over the year.

Impact and Legacy

Impact and Legacy

Impact and Legacy

Market observers are now advising a cautious approach. "Given the current dynamics, it's vital for investors to maintain disciplined long-term strategies. We foresee that volatility will likely persist until there's clearer insight into the economic impact of U.S. tariffs, labor market trends, and Federal Reserve policies, " remarked a senior market advisor.

Investors are encouraged to keep adequate liquidity available for cash flow needs, consider underweighting non-investment grade public debt, and maintain equity exposure aligned with their policy targets. With significant economic decisions on the horizon, the months ahead may hold pivotal changes for market participants.